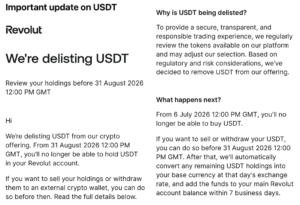

Revolut has notified users that it will delist Tether’s USDT stablecoin by August 31, 2026. Purchases of USDT will be disabled from July 6, deposits will be rejected after July 30, and any holdings not sold or withdrawn by August 31 will be automatically converted into the user’s base currency at the prevailing exchange rate. The company cited “regulatory and risk considerations” without specifying which regulations triggered the decision or whether the delisting applies globally or only in certain jurisdictions. Revolut did not respond to a request for comment on either point.

Revolut holds a MiCA licence as a crypto asset service provider, issued by the Cyprus Securities and Exchange Commission in November 2025 and listed on ESMA’s official register. The delisting follows a pattern established by Coinbase, which began removing USDT from its European platform in 2024 to align with MiCA requirements.

Why Tether Is Being Pushed Out of Europe

Tether has refused to comply with MiCA. The regulation requires stablecoin issuers operating in the EU to hold a portion of their reserves with EU credit institutions — a requirement Tether’s CEO Paolo Ardoino has publicly and repeatedly rejected. Without MiCA authorisation, USDT cannot legally be offered to EU customers by licensed platforms, leaving compliant exchanges and fintechs with no choice but to delist it or risk their own regulatory standing.

USDT remains the world’s third-largest crypto asset by market capitalisation at $184 billion, behind only Bitcoin and Ether. Its closest competitor, Circle’s USDC, holds a $73 billion market cap and ranks fifth. The gap between the two is enormous, but USDC has pursued MiCA compliance while Tether has not.

Tether Chose a Fight With Europe and Europe Is Winning It

The USDT situation in Europe is a regulatory enforcement story playing out in slow motion, and the outcome is becoming clearer by the month. Tether built a $184 billion business operating outside the traditional regulatory perimeter. That worked as long as regulators lacked the tools or the mandate to act. MiCA has now provided both, and every licensed platform that delistsUSDT is a data point in Europe’s favour.

Ardoino’s criticism of MiCA’s reserve requirements is not without merit — forcing stablecoin issuers to park reserves with EU credit institutions introduces counterparty risk that a well-run reserve operation might reasonably want to avoid. But refusing to engage with the regulatory process entirely, while your competitors obtain licences and retain access to the world’s largest single market, is a commercial decision with compounding consequences. Circle is gaining ground in Europe precisely because Tether ceded it.

The broader implication connects directly to the piece on Tether’s $514 million in freezes covered in this publication. Tether is simultaneously one of the most powerful enforcement tools available to US authorities and one of the most resistant actors to formal regulatory oversight. That contradiction is sustainable only for so long. Europe has drawn its line. The question now is how many other major markets follow the same logic — and whether Tether eventually concludes that compliance is cheaper than continued exclusion.