In the wake of global geopolitical and economic instability, where economic sanctions are passed around like hotcakes, confidence in the Dollar as a global reserve currency is at an all-time low. With inflation running rampant nearing 8% YOY, does Bitcoin have what it takes to be a viable global medium of exchange?

After abandoning the Bretton Woods agreement in 1971, thus spelling the end of the gold standard, a new system was born referred to by some as Bretton Woods II. This system relied upon the U.S. dollar being a globally recognized and accepted form of payment, backed by the U.S. economy and enforced by the collective divisions of the U.S. armed forces. With financial liberty at its lowest point in decades, Bretton Woods II finally shows its ugly face. As the global risk of forced asset forfeiture rises significantly, as demonstrated by the Canadian government freezing and seizing assets of the “Freedom Convoy” supporters, Russia threatening seizure of western owned assets in their borders, and the west freezing Russia’s foreign assets and reserves. A need for a Bretton Woods III is upon us.

Historically, human’s first medium, and coincidentally means, of exchange was the Barter system, then came along the use of gold and silver coins which still exist to this day but are mainly used for jewelry and as a store of value. Fast forward a few centuries when the creation of paper currency began. Initially, paper currency was backed by physical gold redeemable from the issuing central bank, known by many as the Bretton Woods agreement. The latest iteration of mediums of exchange is paper currency backed by the economy of each of the issuing central banks; this is known as the Bretton Woods II. Ignoring the monetary, security, and environmental cost of utilizing physical currency, the current Bretton Woods II system possesses major fungibility issues, or the lack thereof. The proposed “Bretton Woods III” would include a “black swan” event where the most widely adopted virtual currency, Bitcoin, is used as an immutable cross-border medium of exchange. To see whether that is even possible, we need to compare Bitcoin transact-ability with the likes of Visa, Mastercard, SWIFT, and SEPA.

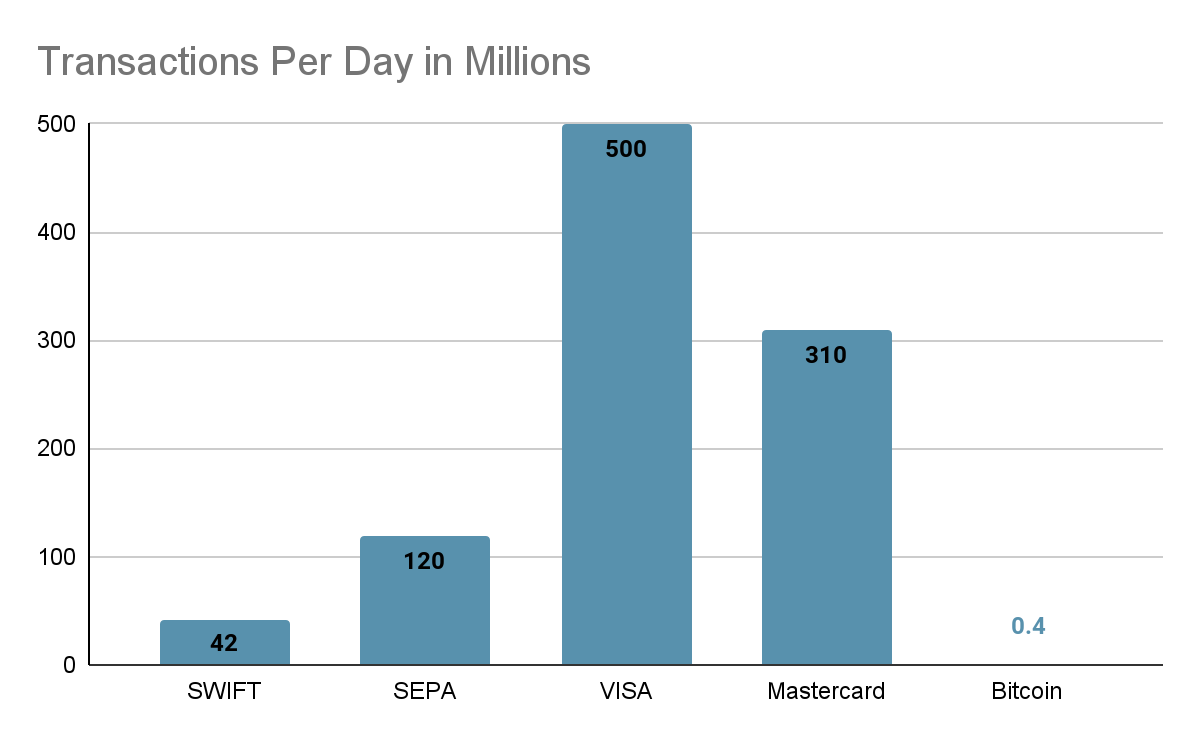

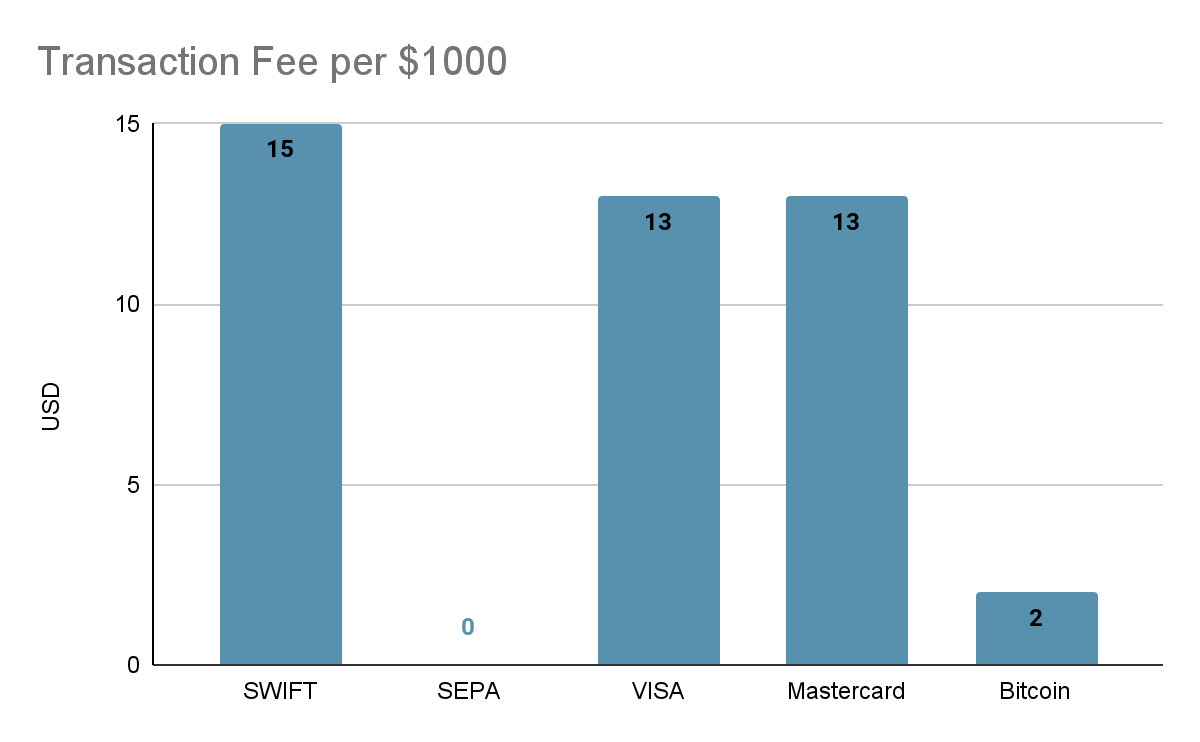

On one hand, the four behemoth financial networks have a combined throughput of nearly 1 billion daily transactions, averaging up to 4 business days for transaction completion. The SWIFT network handles approximately 42M transactions per day with a general fee ranging from $15 to $45. In comparison, SEPA operates upwards of 120M transactions per day and is free of charge, with both services taking anywhere from 1-4 business days to complete. Impressively, Visa and Mastercard handle over 800M transactions per day combined with the transaction taking an average of 2 days to settle, and their fees range from 1.3% to 2.5%. It is good to note that SEPA also offers SEPA Instant, which applies to transfers under €100,000, allowing the user to transfer money in under 10 seconds. Another consideration is that while both Visa and Mastercard take two days to move the funds, authorization for the transaction is instant. It should also be noted that while SEPA transactions are generally free, you would still be required to pay a bank fee for the transfer.

On the other hand, Bitcoin, the most praised crypto hailed as the champion of all cryptocurrencies, has a total throughput of 400,000 transactions per day. Each transaction takes anywhere from 20 to 90 minutes to confirm. While Bitcoin transaction fee fluctuations are often based on network congestions, it has averaged $2 per transaction within the past six months.

Numbers provided by https://www.statista.com/

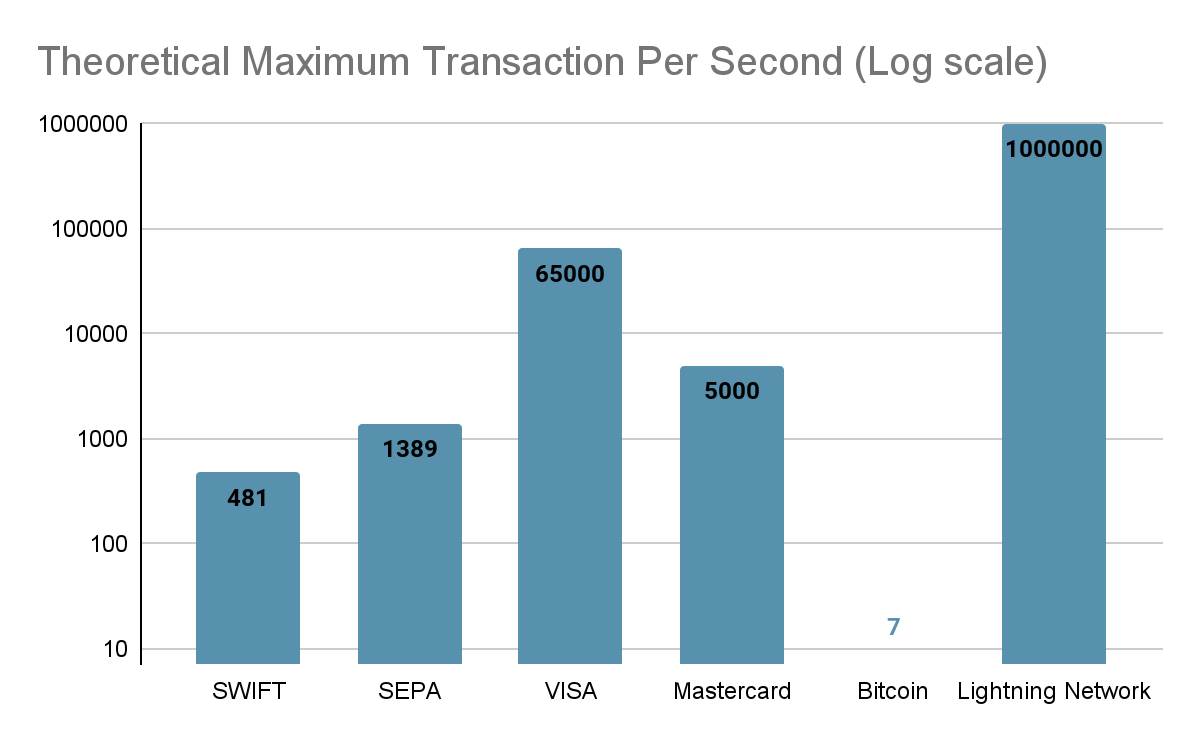

While it may seem that Bitcoin is at a significant disadvantage compared to other major international mediums of exchange in transaction throughput, it may still have an ace up its sleeve. Lightning network, the fast-growing 2nd layer solution built upon Bitcoin to provide off-chain fast and secure transactions, is advertised to handle over a million microtransactions per second while costing 1 Satoshi per transaction, currently equivalent to $0.0004. While this sounds great on paper, it should be noted that the usage of the Lightning Network should be limited to small transactions only, i.e., everyday transactions, as settling transactions off-chain entails greater risk to the user. The excess risk should not be confused with the Lightning network’s security, but when dealing with irreversible transactions, one must always look for the safest option. Lightning Network is only recommended for fast-paced low-volume transactions such as paying a restaurant bill or at a coffee shop, and by doing so, eliminating all the excess noise from Bitcoin’s network. So could Lightning Network be the saving grace of Bitcoin’s quest to be a worldwide means of exchange?

The answer to that is maybe. Although the Lightning Network has been growing fast, being utilized in El-Salvador, where Bitcoin was decreed to be legal tender, it still lacks real-world testing at a massive scale. Lightning may be able to handle El-Salvador’s needs, but the El-Salvador experiment is just a drop in a very large bucket of worldwide money transfer. For Bitcoin to be recognized by major players as a viable medium of exchange, it would have to encourage the adoption of Lightning Network and other 2nd and 3rd layer solutions. That way, the bulk load of usually low-value transactions would be processed by those solutions, ensuring a low enough transaction load for the base network to handle the large-value high security requiring transfers.