The Middle East conflict has thrust energy prices “at the wheel” of global financial markets, creating a stark divide between winners and losers as an oil-driven inflation surge triggers sweeping portfolio reallocations across bonds, currencies and equities.

Soaring oil prices have become the dominant driver across asset classes as investors conduct rapid reappraisals of which economies face greatest exposure to energy shocks and which stand to benefit. The fallout has revived the US dollar from a year-long slump, with traders betting on American economic resilience as an oil producer while simultaneously dumping interest rate cut expectations for import-dependent economies.

Historical Energy Shocks Shape Worst-Case Scenarios

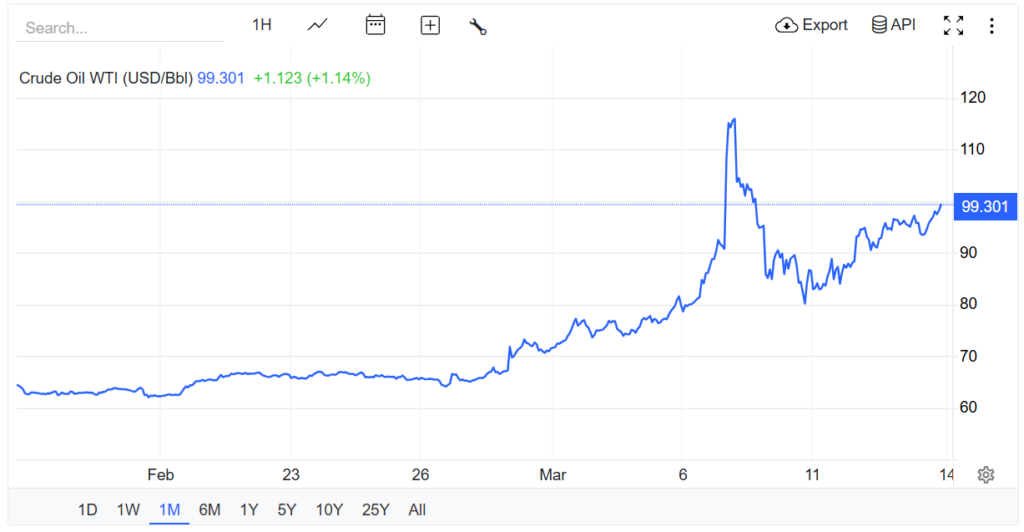

“Energy prices are back in the driver’s seat,” said Jeremie Peloso, strategist at BCA Research. “The disruption level is global.” As the International Energy Agency warned of the “largest supply disruption in history” to the oil market, traders looked to Europe’s 2022 energy crisis following Russia’s Ukraine invasion or the 1979 Iranian revolution oil shock for worst-case economic scenarios.

Record intraday oil price swings have created volatile government bond trading as markets reprice inflation and interest rate paths with each surge and dive in Brent crude. “Oil dominates the short-term narrative,” said Andrew Sheets, global head of fixed income research at Morgan Stanley. “It is so important, and the range of outcomes is so wide.”

Short-term government bonds have borne the heaviest losses as markets price in central bank rate cuts amid inflation fears. This has proven most acute for countries with pre-existing inflation challenges. The Bank of England—facing 3% inflation and UK vulnerability to rising gas prices—is now viewed as more likely to raise rates later this year, compared with two quarter-point cuts priced before the conflict. The European Central Bank is now expected to raise rates once or twice.

Currency Markets Reward Exporters, Punish Importers

“If you’re worried about inflation, it becomes about who loses this race to the bottom,” said Geoff Yu, senior EMEA market strategist at BNY. The US is emerging as a relative winner, with the dollar—which had fallen to a four-year low earlier this year as the Greenland crisis fuelled concerns over President Trump’s policies—experiencing a dramatic revival.

Despite higher rate expectations, the Euro has declined approximately 3% against the dollar since conflict began, falling back under $1.15 and heading for one of its worst months in recent years as investors worry about growth impacts from elevated oil and gas prices. Risk reversals in euro-dollar exchange rates shifted this week to the most bullish dollar position since before last year’s “liberation day” tariff announcement.

Popular trades including dollar shorts and bond market “steepeners”—where investors bet short-term debt will outperform long-dated bonds—have reversed sharply, creating painful losses for macro hedge funds. All major currencies have dropped against the dollar since fighting began, but the worst performers include the South African rand and South Korean won, currencies of two economies most dependent on energy imports, down more than 5% and 3%, respectively.

Emerging markets face a “double blow” from surging oil prices and a stronger dollar, “hitting fiscal budgets, weakening current accounts and stopping further interest rate cuts”, said Mansoor Mohi-uddin, chief economist at Bank of Singapore. Bank of America analysts noted this week that option risk premium in trading the South African rand against the dollar—the extra cost investors pay for insurance against rand declines—has exceeded even that in crude oil itself.

The Canadian and Australian dollars rank among the best-performing major currencies apart from the US dollar, aided by their commodity exporter status and expectations for interest rate increases. Exporter currencies like the Australian dollar have been rare winners on currency markets, while importers such as South Korea have suffered in the broad market shake-out.

Oil Shocks Expose Which Economies Built Resilience and Which Bet on Stability

The violent market reordering triggered by Middle East conflict reveals a fundamental truth: decades of globalisation and energy interdependence created asymmetric vulnerabilities that only become visible when supply chains rupture. Countries that remained energy exporters or achieved self-sufficiency now benefit while import-dependent economies face simultaneous inflation surges, currency collapses and growth slowdowns with limited policy options.

The emerging market “double blow” of higher oil prices plus stronger dollars illustrates why monetary sovereignty matters—when your currency weakens as import costs spike, you’re trapped between raising rates to defend the currency (killing growth) and accepting accelerating inflation. This dynamic explains persistent interest in alternative reserve assets and decentralised financial systems that don’t amplify shocks through currency correlations, though whether Bitcoin actually serves as an effective hedge during energy-driven inflation remains empirically unclear given its tendency to trade as a risk asset during broad market stress.